Your Money

Your Money Which Is the Cheapest Currency in the World? – The Top 10

The Iranian Rial is currently the cheapest currency, followed by the Cambodian Riel. Discover other weak currencies worldwide in our top 10.

Sofia Santos 3/3/2025

International transfers are a tool that allows you to send and receive money between countries securely. Today, we’ll dive deeper into this topic to give you a clearer understanding.

This includes explaining what international transfers are, the types that exist, and how they work. This way, you’ll gain foundational knowledge to handle such transactions confidently.

An international transfer is defined as sending money between bank accounts in different countries. It is commonly used by Mexicans to send remittances and for paying international suppliers or investing abroad.

There are several types of international transfers, each differing in speed, cost, and method.

The main types include:

SWIFT International Transfers: The SWIFT network was created to facilitate communication between banks worldwide. It’s the most widely used by financial institutions globally, enabling international fund transfers.

IBAN Transfer: This International Bank Account Number system is primarily used in Europe, although other countries have adopted it to standardize international bank transfers.

ABA Transfer: A type of bank transfer limited to domestic transfers within the U.S.

Transfers via Financial Apps: Alternatives to traditional banks, offering international transfers with lower fees. Prominent examples include Wise, Revolut, or DolarApp.

The process is as simple as making a typical interbank transfer:

1. Visit the nearest branch of your bank.

2. Inform a representative that you’d like to make an international transfer.

3. Provide the recipient’s details.

4. Specify whether you want to use funds from your account or pay in cash.

5. Confirm the process and keep the receipt.

If you prefer to manage it electronically:

1. Log in to your account via your computer or bank app.

2. Locate the “Transfers” section.

3. Choose the option labeled “International Transfer” or something similar.

4. Select or add the recipient as a new contact.

5. Follow the instructions to complete the process—usually, a confirmation code will be sent to your phone.

Be sure to confirm if your bank offers international transfer services, as not all do.

BBVA and Santander are some institutions that allow such transactions through online banking or apps. Also, be aware of how much banks charge for international transfers.

Generally, when transferring from a traditional bank, it takes:

Up to 24 hours for an ABA transfer.

3-5 business days for international SWIFT transfers.

3-5 business days for SWIFT transfers to an IBAN account.

However, several factors can affect timing:

Destination Country: Some countries have faster banking systems, which can accelerate or delay the process.

Amount Sent: Large sums may require additional security checks.

Currency Conversion: Converting funds to a different currency can add an extra step.

Holidays: Transfers are typically not processed on holidays or weekends, which can delay the transaction.

Another crucial factor is the bank's cut-off time. Transfers made after this time will be processed on the next business day.

Together, these factors determine when the funds will arrive at their destination.

In Mexico, there’s no law setting a maximum limit on international bank transfers. However, financial institutions may have their restrictions. So, check with your bank for specific terms and conditions for your account.

To send money to another country, you must provide certain information about the recipient. The required data will vary depending on the recipient's location.

For example, if you need to transfer money to the United States from Mexico, you’ll need:

The recipient’s bank name and ABA code.

The full name and address of the beneficiary.

The recipient’s account number.

For other countries, you’ll likely need a SWIFT transfer, which requires:

The SWIFT/BIC code of the destination bank.

The beneficiary’s full name and account number.

In some cases, you may also be asked to specify the transfer’s purpose and the currency if it differs from the recipient country’s currency.

Many people are unsure how much banks charge for international transfers, as fees are applied to this service. Costs typically range between 20 and 50 USD, depending on the bank and account type. Some financial institutions, like BBVA MX, offer lower fees under certain conditions—for example, if you complete the transaction yourself via online banking.

Additionally, if the transfer involves a currency exchange, some banks may apply an additional fee for the currency conversion.

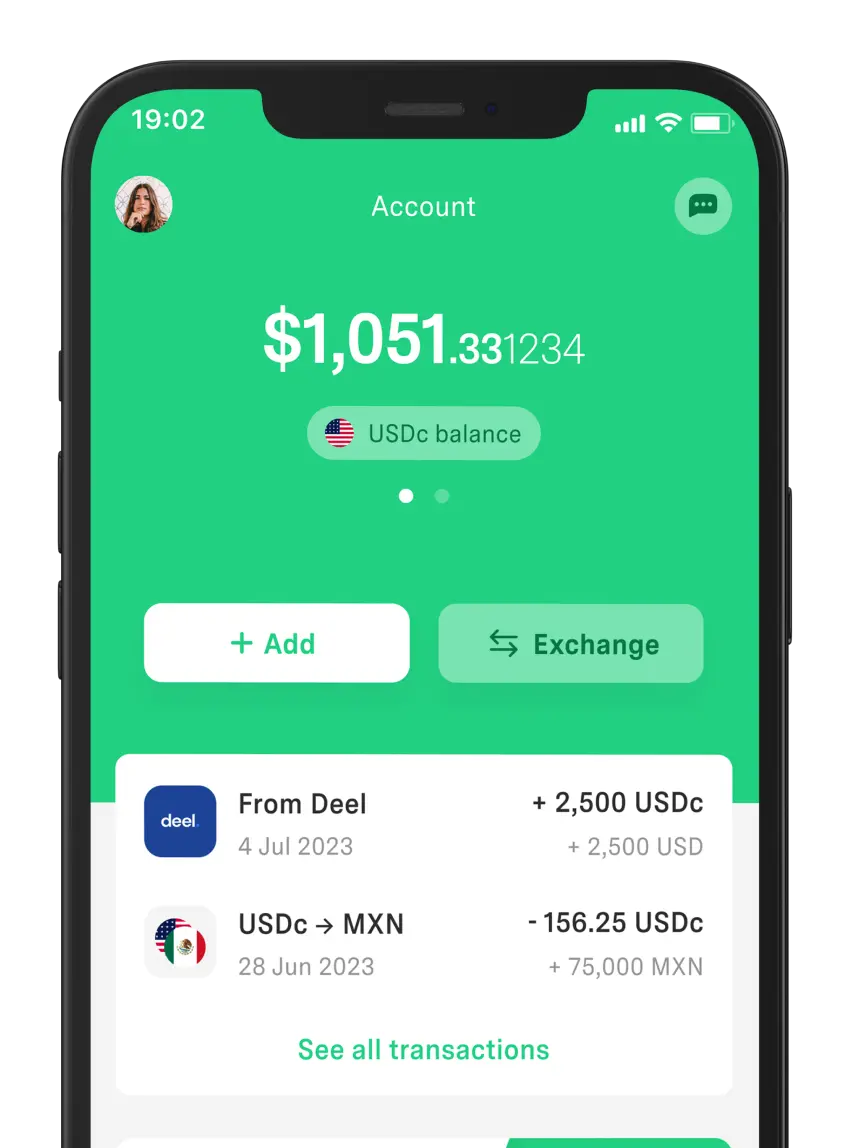

DolarApp is an alternative service for international transfers. First, because it allows you to activate a digital dollar account, and second, because its fees are more favorable than those of typical banks.

Once you’ve activated your dollar account, simply:

1. Open the app: Log in and tap “Send” at the bottom of the screen, then select “Bank Transfer.”

2. Add the recipient: Enter the beneficiary’s full name, bank routing number, and account number.

3. Specify the amount and confirm: Enter the amount you want to transfer, review all details, and confirm to complete the operation.

Another advantage of DolarApp is that you won’t pay extra if you need to convert your digital dollars to Mexican pesos. Just link your MXN account to transfer between currencies seamlessly.

1. Go to the main screen: In the app, locate and select the “Top-Up” button.

2. Choose “Dollars”: Select this option to view your U.S. account information.

3. Copy your banking details: You’ll see the necessary information, including the bank name, address, account number, and routing number.

4. Share: Provide these details to the sender.

DolarApp charges only 3 USD to send or receive money, regardless of the amount.

For these transactions, banks typically generate a reference code after completing the transfer. To track the status of the transfer, simply log in to your bank’s online portal and enter the code.

On platforms like DolarApp, the process is even easier, as you can check the transaction history to verify the status.

If you’re using a financial institution in Mexico, you may need to track the transfer via the Interbank Electronic Payments System (SPEI), as it follows the Bank of Mexico’s system.

To track it through SPEI:

1. Go to the website https://www.banxico.org.mx/cep/.

2. Enter the transaction details, such as the tracking key, sending bank, and receiving bank.

3. Once you’ve filled out the form, click “Check Your Payment” to see the transfer’s status.

BBVA also allows you to manage and monitor your transactions online, by phone, or at a branch location.

The world has borders. Your finances don’t have to.

Your Money The Iranian Rial is currently the cheapest currency, followed by the Cambodian Riel. Discover other weak currencies worldwide in our top 10.

Your Money

Your Money Learn to differentiate between the statement closing date and payment due date on your credit card to maximize its benefits when making purchases.

Your Money

Your Money Interest rates are a crucial factor that influences every step of your financial journey. We explain their definition and how they work

Scan the code and join the global movement