Your Money

Your Money Annual Tax Return 2025: What You Need to Know

Now that it’s already 2025, it’s time to get ready to file your taxes for the 2024 fiscal year. We have all the details right here.

Santiago Sanchez 4/21/2025

Sending money from one account to another may not be too complex, but it’s important to know the requirements so the transaction goes smoothly—whether it’s for personal payments, business purposes, or shopping.

Especially since they can vary based on the bank or transfer type. For that reason, we’ve prepared an informative article to help you figure out exactly what you need to succeed.

In a nutshell, you need a bank account or card, the recipient’s info, and the funds. However, requirements can differ according to the payment method and the bank in question. Still, there are some general factors to keep in mind:

An active bank account. It is essential to have an active account with the bank from which the bank transfer is to be made.

Access to online or mobile banking. Every financial institution in Mexico offers some sort of digital banking for these transactions, so be sure you have your login and password set up (either from your computer or smartphone).

Beneficiary details. You’ll need the full name and account number or CLABE interbancaria of the receiving bank. For international transfers, you need the SWIFT/BIC code.

Sufficient balance. Naturally, you must have enough funds in your account to cover both the transfer amount and any possible fees.

With these items in hand, you can move on to the next step: how to make a bank transfer.

Imagine you’ve just completed an online transfer—how can you verify it was carried out correctly?

Whether you did it via the mobile app or e-banking, the system will generate a confirmation. This is the proof you’d need in case of any dispute, so it’s wise to download it or keep a copy. You can also review the transaction history in your account to confirm the amount was deducted. That lets you verify the procedure and show the payee that it’s done—especially useful if you’re unsure how long the transfer might take to appear.

SPEI is the platform specifically designed for electronic transfers between banks. Its name is an acronym for Sistema de Pagos Electrónicos Interbancarios (Interbank Electronic Payment System), created by Banco de México.

Through SPEI, you can send or receive money regardless of whether the accounts belong to different financial institutions.

Among its advantages:

Transfers that are both quick and secure.

Available 24/7.

Handles any amount—from small sums to large transactions.

To use it, you need:

A bank account that supports SPEI. Most financial institutions provide this service—sometimes with a monthly or per-transaction fee.

Beneficiary’s details. Including their full name, CLABE interbancaria, card number, or phone number linked to the bank account, plus the receiving bank.

In certain institutions, you first have to register the beneficiary’s account.

This tool is key for managing your finances and making payments in Mexico—whether personal or business. Now let’s see in practice how to do an electronic transfer.

This type of transfer is used when you want to send or receive money from a different bank.

Here are the steps:

1. Log in with your credentials. Access your bank’s website using your username and password.

Note that if it’s your first time sending money to a new contact, some banks will require you to register that account in advance. Others have you wait about 30 minutes before sending money after you add a new payee.

2. Go to the transfers section. Look for the “Transfer” menu or something similar.

3. Choose interbank transfer. Click on the tab that pertains to other banks and select the destination.

4. Enter the amount and reason. Input the sum to be sent, plus any description you want to appear on the transaction record (if required or if you’d like).

5. Confirm and authorize. Double-check you typed in the correct details, then finalize using your token or SMS code.

When the operation is finished, download and keep the proof of transfer.

If you prefer a teller-window transaction, you need the same basic requirements, plus physical ID and the money itself. Typically, you’ll bring:

Official ID. Any valid ID, like your voter card (INE) or professional license.

Beneficiary data. That person or company’s full name, account number, interbank CLABE, or card number.

Sum to be transferred. Let the teller know how much you’re sending. You’ll need sufficient cash or a bank account to draw from.

You can do this at the closest bank branch, or sometimes in authorized places like pharmacies, supermarkets, or convenience stores. Don’t forget to ask for and keep the receipt as evidence that the operation was carried out.

Wondering how to do a bank transfer from your phone?

You have two ways: through the official mobile banking app or through DiMo.

So, what do you need for each?

1. Via Mobile Banking App

Download and activate the bank’s official mobile app.

Have the recipient saved or add them with their name, CLABE, account number, or card number.

Sufficient balance in your account.

A token, password, or SMS code (depending on the bank) to authorize operations.

A stable network connection to finalize the transfer.

After finishing, feel free to share the receipt with the payee.

2. Via DiMo

A DiMo-enabled account from an institution that offers it.

The DiMo app on your phone, registered with your personal data and bank account.

The beneficiary’s phone number.

An adequate balance in your account.

Unlike traditional transfers, you only need the beneficiary’s phone number.

There’s no universal cap on bank transfers; it usually depends on each bank’s policies as well as your account type.

For instance, at Citibanamex, you can move up to 500,000 MXN daily, whereas at other banks (like BBVA), no specific standard limit may be set.

You should note that if you get over 15,000 MXN monthly in your banking app, the bank will inform the SAT. Still, they don’t directly oversee your electronic transfers.

High bank fees and local exchange rates for international transactions can weigh on your finances. Thankfully, we present a more wallet-friendly solution for sending or receiving foreign currency transfers.

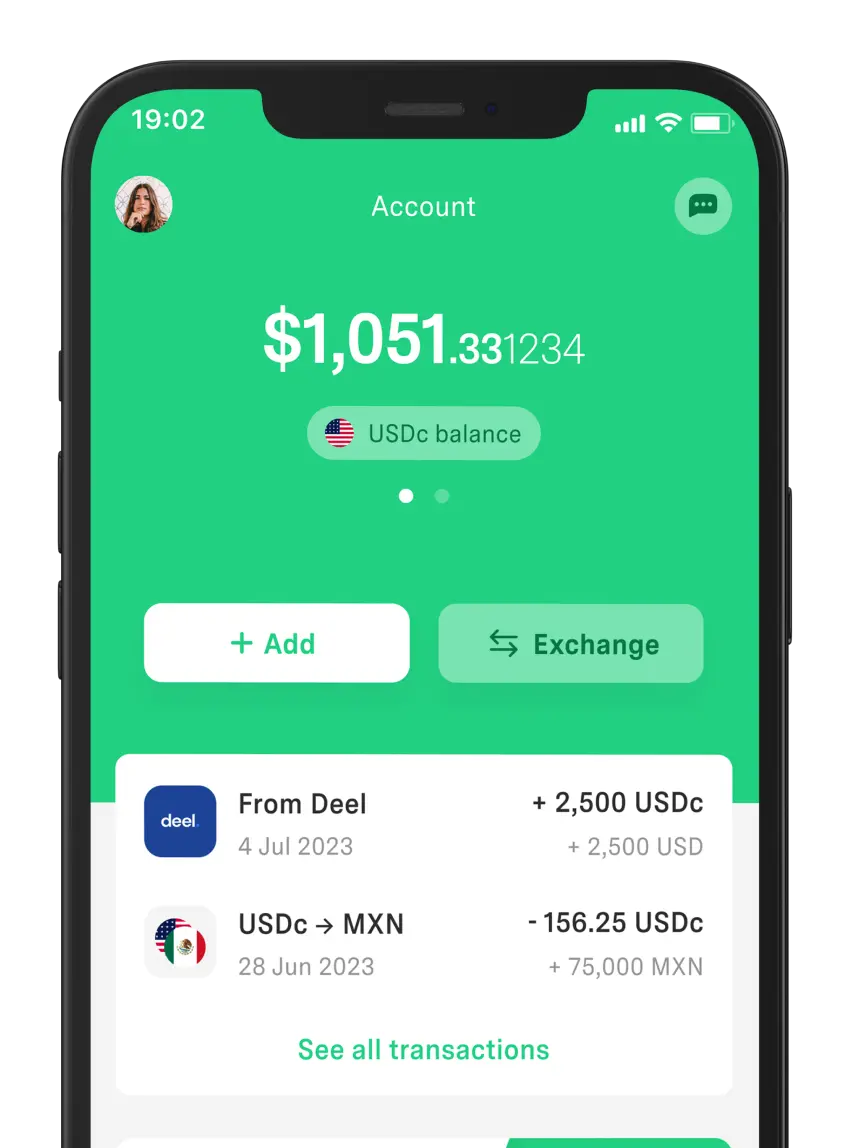

Enter DolarApp, our financial platform that pairs advanced technology with global banking services.

First, it lets you do everything from a user-friendly app: get account details in digital dollars, send/receive money, or convert pesos to USDc (and vice versa) at a competitive exchange rate.

Other advantages of DolarApp:

No fees for converting your money between pesos and digital dollars.

A standard $3 USD cost per transaction, no matter the transferred amount.

With DolarApp, you can streamline international remittances while saving time and money. It’s an option worth considering, wouldn’t you say?

The world has borders. Your finances don’t have to.

Your Money Now that it’s already 2025, it’s time to get ready to file your taxes for the 2024 fiscal year. We have all the details right here.

Your Money

Your Money Banks usually define a limit for bank transfers, but there are additional aspects you need to know.

Your Money

Your Money A bank account usually has 10 digits, but which number should you provide so you can be paid? The bank account number or the CLABE? We explain.

Scan the code and join the global movement