Your Money

Your Money Which Is the Cheapest Currency in the World? – The Top 10

The Iranian Rial is currently the cheapest currency, followed by the Cambodian Riel. Discover other weak currencies worldwide in our top 10.

Sofia Santos 4/29/2025

In banking transfers, there are two key elements for transaction security: the reference number and the payment concept, whether domestic or international.

Each has a specific purpose and it’s vital to understand how they work to avoid errors or issues.

That’s why in this post we’re giving you a definition of what a reference in a transfer is, along with some examples of its use. We’ll also explain what the concept of a transfer is and the benefits both provide in banking transactions.

It’s a number or code that allows you to specifically identify each banking transaction. However, in certain systems or configurations, it may accept text or alphanumeric combinations.

The reference for a bank transfer is often confused with the concept, but they are two different fields.

The reference in a bank transfer is a number automatically generated by the system. Sometimes, though, it must be entered manually by the sender, such as when the bank requires a specific number related to an invoice or contract.

It all depends on the bank’s policies.

The bank reference number is the code used to identify a particular transaction. Additionally, it varies according to the system or the financial institution and can include important information related to the transfer, such as:

Invoice number

Recipient’s account number

Date of the transaction

Contract number

In general, it appears on the receipt or in the details of your transaction in online banking.

What is it for?

It’s used to identify, track, and verify each operation in a unique way, facilitating control and the resolution of possible problems.

Bank reference number example:

In Mexico, a bank reference number might look like “0067345” through the SPEI system.

But in the case of international transfers, such as those made via SWIFT, the reference could be the UETR, i.e., an alphanumeric code of 36 characters that allows global tracking.

It’s an optional text where the sender can add a description or reason for the payment. It’s placed when making a bank transfer and provides the recipient with additional context about the purpose of the transaction.

This detail allows you to quickly identify the reason for the transfer, in both personal and commercial transactions.

It can contain text as well as numbers.

The most important thing about this field is that the recipient instantly understands what the payment is for.

Examples of transfer concepts:

Personal payments | Commercial payments | Recurring transfers |

“Rent January 2025”. “Loan repayment” | “Payment for January services” “Advance payment for contract X” | “Auto loan payment”. “Monthly loan installment”. |

The goal is for the receiving party to understand the nature of the payment at a glance.

The aim is to include relevant, understandable details for the recipient while avoiding unnecessary or sensitive information. Nor should you write suspicious words or phrases that have nothing to do with the true purpose of the payment.

Keep in mind that banking monitoring systems use technologies that detect potential illegal activities. Therefore, if the SAT sees unusual or inconsistent concepts, they might request detailed explanations and, in more serious cases, demand evidence proving the transaction’s legitimacy.

Not recommended concept examples for a transfer:

“Thanks for everything”

“Undeclared loan”

“Secret gift”

“Drugs”

“Weapons”

“Cash business”

Think carefully about which concept to include in a transfer so you don’t have to provide unnecessary explanations.

The fields for the concept and reference in a transfer help you organize your payments and optimize key processes.

Technical tracking: As it’s a unique number, it allows quick tracking and verification of transactions within the banking systems.

Accurate reconciliation: It facilitates the technical identification of each transfer for the receiving party, which is useful to avoid duplicates or errors.

Banking organization: Serving as a unique identifier, it ensures each transaction is recorded and associated with the corresponding payment in the correct way.

Clear identification of purpose: Lets the sender explain the reason for the payment, helping the beneficiary understand what the transaction is about.

Streamlined business reconciliations: By including information such as invoice numbers or specific descriptions, it assists accounting departments in verifying and organizing payments.

Detailed history: It acts as a clear record of the payments made, aiding in both personal and business follow-ups.

Reduced confusion: Minimizes misunderstandings or issues in identifying the payment.

We could say that the reference number in a transfer and the concept enhance security and clarity in your transactions.

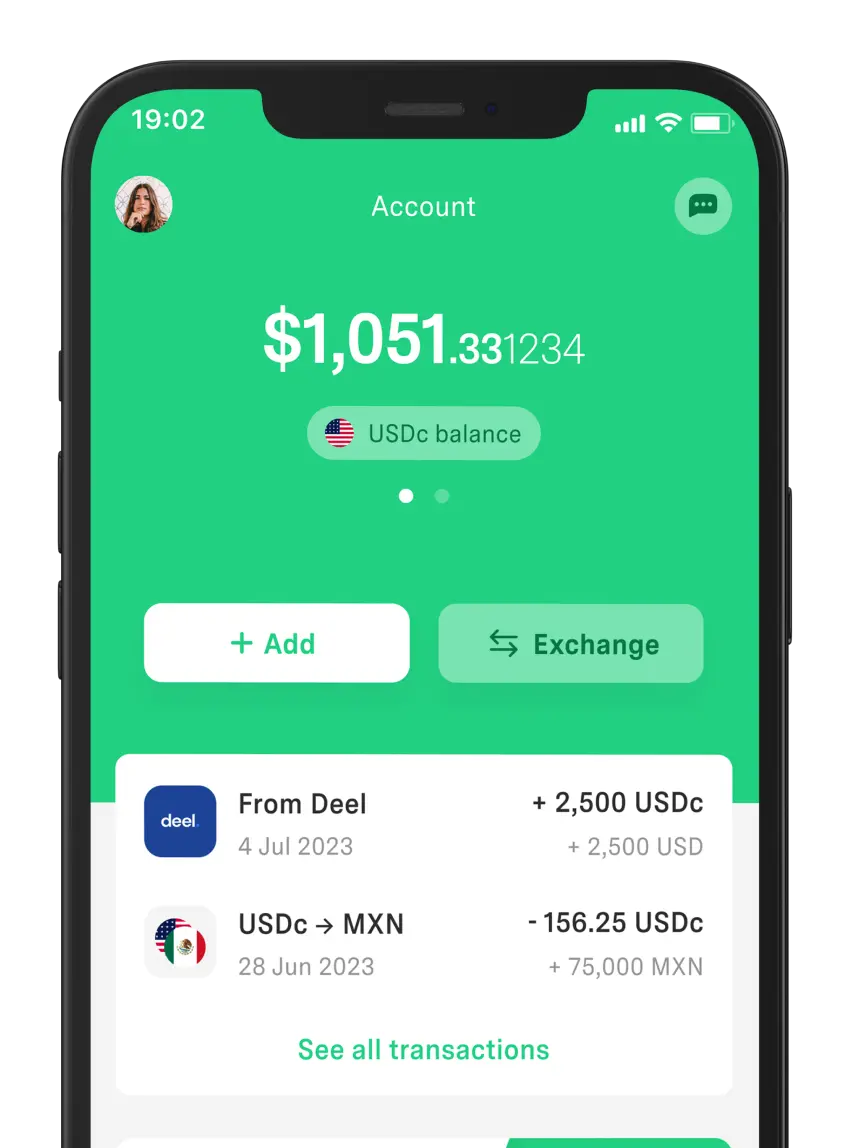

Now, if you perform international transfers, consider using DolarApp to simplify your financial operations. With it, you can send or receive money in digital dollars and convert them to pesos with a favorable exchange rate. This way, you can simplify your electronic payments while maintaining security.

Both the recipient and the sender can view the reference in a bank transfer. Likewise, financial institutions use it internally to identify and track the transaction.

In Mexico, the reference number in a transfer can be up to 7 digits through the SPEI system. But the length often varies between banks or transfer platforms. For example, the reference in a BBVA transfer can be 20 to 30 digits.

To complete a bank transfer, you need information such as the recipient’s full name, account or CLABE number. As well as the amount to transfer and the tracking key generated by the bank.

The world has borders. Your finances don’t have to.

Your Money The Iranian Rial is currently the cheapest currency, followed by the Cambodian Riel. Discover other weak currencies worldwide in our top 10.

Your Money

Your Money Mexico's coins and banknotes are subdivided into centavos and pesos. Family C, C1 and D has the current coins and G has the most recent banknotes.

Your Money

Your Money Now that it’s already 2025, it’s time to get ready to file your taxes for the 2024 fiscal year. We have all the details right here.

Scan the code and join the global movement